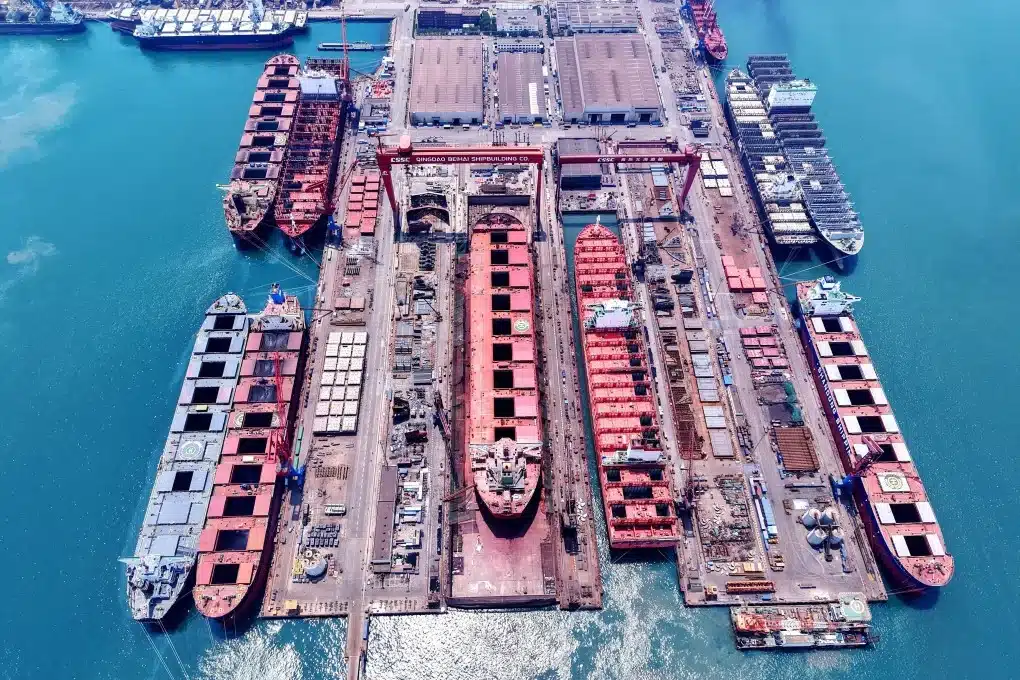

China’s Shipbuilding Sector Maintains Global Dominance in 2025

China’s shipbuilding industry has once again solidified its position as the world’s leader, achieving remarkable results across three key metrics for the 16th consecutive year in 2025. According to the Ministry of Industry and Information Technology, China’s shipbuilding output reached an impressive 53.69 million deadweight tonnes (DWT), accounting for 56.1% of the global total. Additionally, new orders surged to 107.82 million DWT, representing 69% of the global market, while holding orders stood at 274.42 million DWT, making up 66.8% of the market share.

This sustained growth underscores the integral role of China’s manufacturing sector in the global economy. Li Yanqing, vice president of the China Association of the National Shipbuilding Industry, noted a significant return of international shipowners to the Chinese market. In 2025, a staggering 89.6% of China’s shipbuilding output was destined for export, with 89.5% of new orders and 93.2% of holding orders also earmarked for international clients. These figures highlight China’s pivotal role in global shipping, with nearly nine out of ten ships built in the country serving the international market.

Factors Behind China’s Shipbuilding Success

Several factors contribute to China’s attractiveness to shipowners worldwide. Speed and efficiency are paramount. Hudong-Zhonghua Shipbuilding, a subsidiary of China State Shipbuilding Corporation (CSSC), has been delivering liquefied natural gas (LNG) carriers for QatarEnergy’s transportation project with remarkable regularity. Following the first delivery in 2024, vessels have been arriving almost monthly, exceeding expectations, according to Saad Sherida Al-Kaabi, Qatar’s minister of state for energy affairs.

Value for money is another critical aspect. Zhong Zhechao, founder and CEO of One Shipping, emphasized that China’s mature and fully integrated shipbuilding industrial chain provides a competitive edge. Chinese shipbuilders can offer large-scale construction, reliable delivery schedules, and innovative green vessel solutions, all while ensuring access to financing support. This combination helps shipowners manage risks associated with technology, funding, and delivery.

Xu Guangjian, a professor at Renmin University of China, pointed out that China’s systemic competitiveness across the entire shipbuilding industrial chain is a key factor in its success. As the only nation with all industrial categories listed in the United Nations classification, China’s manufacturing value added accounts for 30% of the global total. This robust manufacturing system allows Chinese shipbuilders to maintain production stability even amid global supply chain disruptions, providing international shipowners with peace of mind.

Innovations and Future Prospects

China’s shipbuilding industry is not only focused on quantity but also on quality and innovation. The construction of the Adora Flora City, China’s second domestically built large cruise ship, is currently over 91% complete, nearly eight months ahead of schedule. This efficiency is attributed to the use of AI-driven scheduling algorithms, which have increased production capacity by 25%.

U.S. Struggles to Compete with China’s Shipbuilding Dominance

Moreover, the industry’s commitment to green transformation is evident in the delivery of world-class green and intelligent vessels in 2025. A CSSC executive noted that Chinese enterprises are expanding their global strategies, enhancing localized services and supply chain networks to gain recognition from international clients.

The structural evolution of China’s shipbuilding sector is noteworthy. Transitioning from a focus on medium- to low-end ships, the industry has made significant strides in high-end vessel types, including LNG carriers and large container ships. In 2025, six Chinese shipbuilders ranked among the world’s top ten in all major indicators, with CSSC emerging as the largest listed shipbuilding company, holding 18% of global orders.