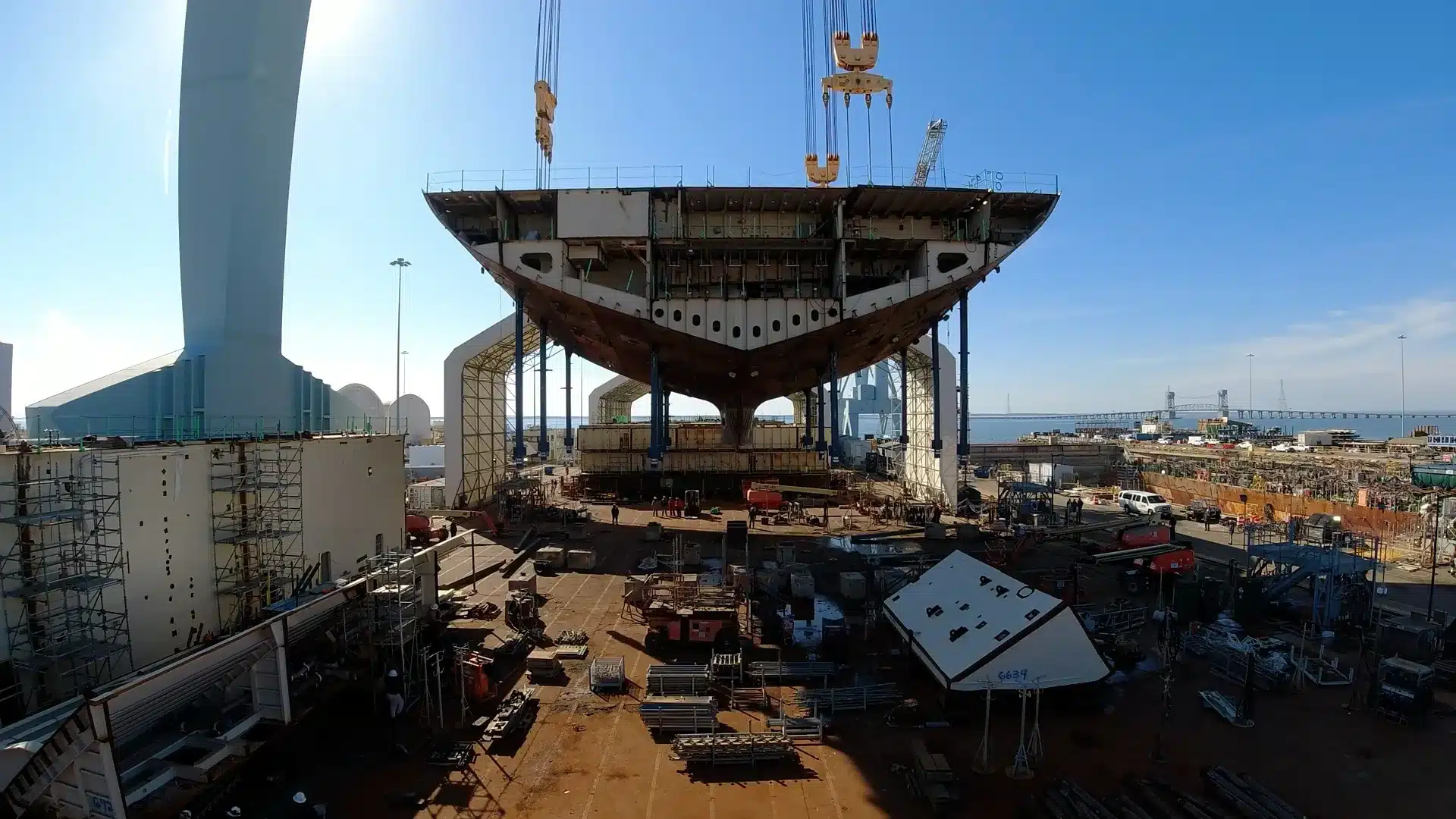

US Shipbuilding Faces Urgent Challenges

In 2024, the United States accounted for a mere 0.1% of global commercial shipbuilding output, a stark contrast to China’s dominance, where the China State Shipbuilding Corporation delivered more commercial tonnage than all US shipyards combined since World War II. Despite US ports processing 6% of global container traffic, the nation ranks 22nd among global flag registries and only transports 0.2% of this traffic. Recognizing the need for a competitive shipbuilding industry, the US aims to enhance both economic and national security through strategic investments and modernization efforts.

Challenges Facing US Shipbuilding

The US shipbuilding industry is grappling with a multitude of interconnected challenges that hinder its competitiveness. Complex regulations, funding shortfalls, and a limited workforce contribute to slow and costly production processes. Additionally, the industry has become overly reliant on naval contracts, which has stunted commercial growth. While subsidies have been a temporary lifeline for US shipyards, they do not foster long-term competitiveness. Unlike global leaders such as China and South Korea, the US lacks state-owned shipbuilders and large conglomerates capable of absorbing industry losses, making it difficult to replicate their subsidy-heavy models.

To revitalize the shipbuilding sector, the US must explore emerging opportunities in autonomous shipping, alternative fuels, and smart ports. These disruptive segments are reshaping the maritime industry and can generate significant demand across the maritime value chain. By leveraging existing strengths in technologies like artificial intelligence and the Internet of Things, the US can attract private investment and create a more sustainable maritime industrial base. This approach not only aims to boost trade but also to maintain naval capacity by keeping shipyards and suppliers engaged during periods of fluctuating demand.

Historically, the US shipbuilding industry has struggled to adapt to changing market dynamics. The transition from wood to steel in the mid-1800s was slow, and subsequent efforts to rebuild the industry in the 1970s faltered due to economic pressures. Today, structural inefficiencies, such as higher input costs and a smaller protected market, continue to constrain the competitiveness of US commercial ships against leading Asian producers.

Strategic Recommendations for Future Growth

To address these challenges, the US must implement a strategic plan that focuses on developing new markets and attracting private investment. This includes creating a Maritime Security Trust Fund to pool resources and encourage multi-year planning for maritime security and resilience. Additionally, linking funding to common technical specifications can help unlock scale and stimulate private sector investment.

Investing in talent development is also crucial. By creating apprenticeships and scholarships in fields related to autonomy, alternative fuels, and smart ports, the US can build a skilled workforce that meets the demands of a modern maritime industry. Furthermore, modernizing regulatory frameworks to support innovation in autonomous vessels and alternative fuels can accelerate the adoption of new technologies.

Finally, the US should focus on building allied demand for its maritime products. By promoting open, interoperable smart port technologies and establishing partnerships for co-production, the US can expand its market share and strengthen its position in global trade. The time to act is now; delaying could allow competitors to seize the opportunities that lie ahead in the evolving maritime landscape.