Shipping Markets: Summer Was a Mixed Bag

The shipping market had a mixed performance over the summer period. In its latest weekly report, shipbroker Xclusiv Shipbrokers said that “summer moved on and September is “ante portas” but things remain quite unchanged. The Chinese economy is still struggling to find her footsteps after the end of the zero Covid policy. China’s numbers concerning steel, iron ore, coal and soybean have improved compared to the same period last year, but this seems not enough to create the conditions for a dynamic upward trend in the dry market freight rates”.

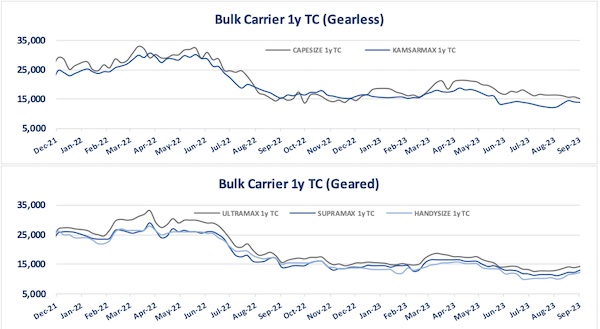

“The BDI was at 1,086 points on 31st August 2023, almost 13% higher from the same day in 2022. The index was mainly supported by the Cape and Panamax rates as the BCI 5T/C was at USD 9,072 and the BPI 5T/C was at USD 13,526, increased by 262% and 23% respectively on yoy basis. The BSI 10T/C and the BHSI 7T/C on 31st August 2023 were 41% down each compared to the same day of 2022. The lack of an upward trend in the horizon has also pushed dry vessels prices into a correction. Prices for a 10-year-old Japanese Supramax are about 24% lower than the same period last year, while 5-year-old Chinese Ultramax’s have seen a correction of about 12%. Finally, prices of 10-year-old Chinese Capes have seen a correction of about 20%”.

Source: Xclsuiv

According to Xclusiv, “the Chinese property sector has received another blow as another major construction company – Country Garden Holdings Co. – is facing the danger of default. The company, China’s sixth largest developer by sales, warned that it may default on its debt and raised concerns about staying in business after the Chinese developer posted a record first-half loss of almost $7 billion. Chinese authorities are still trying to figure how to successfully support the property sector as all the measures taken until now didn’t bear any fruits. In an attempt to further support the economy, the People’s Bank of China has announced plans to cut the required level of financial institutions’ foreign exchange reserves this month in the latest move by Beijing to combat depreciation of the Yuan. The Central Bank said it would lower China’s foreign exchange reserve requirement ratio from 6 per cent to 4 per cent, effective September 15, “in order to improve the capacity of financial institutions to use foreign exchange funds””.

“Moving from Dry to Wet, Russia surprised the market by coming to an agreement with its OPEC+ partners on further cuts to its crude exports. The plan until now was a reduction of crude oil exports by 500,000 barrels/day in August and then taper the reduction to 300,000 barrels a day in September, but now it seems that the September export reduction is probably continuing into October. Russia, one of the two de-facto leaders of the Organization of Petroleum Exporting Countries and its allies, issued the statement amid an expected extension of Saudi Arabia’s one million barrel-a-day oil supply cut into October”, the shipbroker noted.

Source: Xclsuiv

Xclusiv added that “in the Asian markets, the appetite for US crude oil is growing. The US crude oil market share grew to a record of 7% in Q2 2023, up from an average of 5.8% in 2022. India, a major Asian importer has long switched towards Russia for cheaper crude oil while other countries like Taiwan and Thailand have not only filled the gap left by India but have also replaced Middle Eastern sources with US ones. In China, the government has issued more than 95 million barrels export quotas for clean oil products helping oil companies to implement their export plans for September. Export quotas for fuel oil are used to supply bonded bunkering at China’s ports with domestically produced barrels. As the domestic recovery is slower than expected, it is possible for the government to issue more export quotas to spur GDP growth in the rest of 2023”, the shipbroker concluded.

Nikos Roussanoglou, Hellenic Shipping News Worldwide